A Unified DeFi Ecosystem: Paradex Exchange Paradex Chain, XUSD (Native Synthetic Dollar), powered by $DIME.

.svg)

Imagine sitting at a poker table where your opponent gets a free last look at your cards before deciding to call or fold. You’d never agree to such a game, yet that’s effectively how many on-chain exchanges operate today. And oftentimes, these are the exchanges we all rave about, such as Hyperliquid. In the current decentralized perps markets, high-speed market makers enjoy a “free last look” at your trades, canceling their orders last-second if the trade would be unprofitable for them. It’s as if the house never loses – and you’re not the house. This structural imbalance is invisible to most users (the UI feels fast, after all), but it shows up in subtle ways: ever notice how you’re instantly down a percent or two after a perp trade on some DEXs? That’s your opponent peeking at your hand. Paradex’s core thesis is that they can build a better game, one where trading is fair by design, not by how fast you are. After all, isn’t the point of crypto to level the playfield to give the little guy a shot?

Key Takeaways

Paradex's Core Problem & Vision

Current on-chain exchanges give market makers a "free last look" (cancel-priority), leading to unfair execution and slippage for retail users. Paradex rejects this TradFi copy-paste model and instead designs from first principles, focusing on fairness, privacy, and deterministic settlement.

Market Structure Innovation

Retail Price Improvement (RPI): A special lane for retail traders that gives them inside-spread prices and zero fees, while insulating makers from toxic flow. Request for Quote (RFQ): Allows large/institutional traders to execute block trades privately and atomically, avoiding slippage and front-running. Together, RPI + RFQ create segmented flow, eliminating the latency arms race and making liquidity more sustainable.

Privacy as a Feature

Paradex introduces hidden retail orders, encrypted positions, and off-chain matching to prevent MEV, front-running, and information leakage. Privacy is positioned as non-negotiable for attracting institutional capital on-chain.

ZK-Rollup Infrastructure

Built on a CairoVM-powered zk-rollup, ensuring deterministic finality, scalability, and composability while settling securely on Ethereum. Separation of roles: Ethereum acts as the "court of law" (final settlement), Paradex chain as the "government" (flexible execution).

Unified Trading & Capital Efficiency

Portfolio margin across spot, perps, and options for true capital efficiency. Innovative products: Perpetual Options (no expiry, continuous funding), synthetic stablecoin XUSD, and Vaults for passive strategies. Blends roles of broker, bank, exchange, and asset manager — creating a "prime brokerage on-chain."

Business Model & Revenue Streams

Zero taker fees → revenue from Payment for Order Flow (PFOF) paid by market makers. Additional revenue from: Net interest on deposits, Borrow/lend spreads, Vault management fees, Stablecoin yield, Platform/app-store style fees. Paradex's pitch: "Binance-level spreads, zero fees."

Tokenomics ($DIME)

Designed to avoid the "high FDV, low float" trap. Insider tokens tied to performance milestones (not just time-based). Revenue sharing via buybacks & burns, eventually turning $DIME into an equity-like asset. Long-term goal: make $DIME attractive to both retail and institutions through fundamental value accrual.

Summary

The Paradex Thesis positions Paradex as a third-generation on-chain exchange, breaking away from TradFi replication and instead leveraging crypto's native advantages: zk-proofs, flow segmentation, and protocol-level privacy. By combining fair execution (RPI, RFQ), deterministic zk-rollup settlement, capital-efficient portfolio margining, and a multi-stream business model, Paradex aims to deliver Binance-level spreads at zero fees while unlocking new product classes like perpetual options and on-chain vaults. Its token, $DIME, is structured with long-term insider alignment and revenue buybacks, seeking to restore credibility to exchange tokens.

Conclusion: Paradex is a high-conviction bet on a fairer, more institution-ready DeFi exchange. While execution and distribution risks remain, its design represents a zero-to-one leap in exchange architecture that could set a new standard for on-chain markets.

Disclaimer: The author of this report is not currently being paid by Paradex and does not currently have any vested interest. The author has not purchased or sold any token for which the author had material non-public information while researching or drafting this report. These disclosures are made consistent with Delphi's commitment to transparency and should not be misconstrued as a recommendation to purchase or sell any token, or to use any protocol. The contents of each of these reports reflect the opinions of the respective author of the given report and are presented for informational purposes only. Nothing contained in these reports is, and should not be construed to be, investment advice. In addition to the disclosures provided for each report, our affiliated business, Delphi Ventures, may have investments in assets or protocols identified in this report. These disclosures are solely the responsibility of Delphi Ventures.

We’re seeing two divergent philosophies in the race to build high-performance on-chain exchanges:

This camp, exemplified by projects like Hyperliquid (and some Solana-based DEXs), mimics centralized exchange mechanics as closely as possible. It means ultra-low latency networking, matching engines with strict price-time priority, and tricks like cancel-priority or speed bumps to protect market makers. Essentially, they bring the NASDAQ playbook on chain, even if it requires custom sequencers or semi-centralized infrastructure to achieve speed. Hyperliquid, for instance, uses custom block building logic that prioritizes cancels over GTC and IOC orders. This gives makers confidence to quote tighter and gives takers the illusion of immediacy. It feels snappy: takers usually get filled if liquidity is shown, and makers feel safer quoting. But this is essentially a patch over a deeper issue. Cancel-priority is a double-edged sword: it cuts down on outright sniping of makers, yet it grants makers a perpetual option for a “free last look” to never trade at a loss (they can always cancel if the market moves against them). In other words, it’s like the house always getting to peek at your hand and fold when it’s not in their favor. Makers will indeed show tight prices on the screen, but as a taker you’ll rarely get those nice prices, the moment your trade would be a great deal for you, the maker cancels. What remains is slippage: the delta between the price you see and the price you get filled at, because makers were able to pull their quotes before you can get filled. This dynamic leads to a cat-and-mouse latency game: quote tight, get pinged by a fast taker, cancel, repost, repeat. It produces cancel spam, flickering quotes, and ultimately wider effective spreads for any participants who aren’t algos. It’s a high-speed game that works well for HFT firms but leaves normal users at a disadvantage. Camp A’s ethos is essentially “if it ain’t broke, don’t fix it”, copy traditional market structure to on-chain, even if that means running a semi-centralized fast path. This model also might not scale well as blocktimes reduce as your time to cancel advantage is eroded.

This is Paradex's camp. Instead of assuming the traditional model is optimal, Paradex is redesigning the playing field itself by embracing crypto's unique strengths: on-chain validity proofs for trustless execution, protocol-level privacy, and new order types like RPI and supplementary execution protocols like RFQ to execute large and complex trades with atomic leg execution. This first principles approach changes the game to make it fairer for a broader range of participants. This camp acknowledges that blockchains are not NASDAQ and shouldn't try to be; they have different constraints and superpowers. By using cryptography and thoughtful design, Paradex avoids the latency arms race altogether and eliminates the "free last look" option. The idea is to bake fairness into the protocol, rather than relying on centralized speed or bandaid rules. Paradex's approach is admittedly more radical and involves more execution risk, but it aims to unlock a new wave of users, especially institutions, who have so far avoided DeFi due to issues like toxic flow and lack of privacy. Wall Street doesn't just need fast execution, they need trustworthy execution and the ability to trade without broadcasting their hand to the entire world.

Both camps ultimately want to attract real trading volume on-chain. But I'm convinced Camp B's approach is more likely to unlock the next wave of adopters, especially institutional players who have so far dabbled in CeFi but largely avoided DeFi. Why? Because Wall Street doesn't just need fast execution; it needs trustworthy execution and privacy. A paradigm that offers deterministic trade finality, privacy for large orders, and protection against toxic flow is more appealing to an institution than one that says "we're just like your current exchange, except running on a potentially unstable blockchain, favoring whoever has the fastest bot, and we won't make you KYX/AML." Paradex's bet is that a slightly different design, one that breaks from TradFi orthodoxy in key areas, will ultimately win the confidence of traders who want to do size on-chain without fear. It's a different road to the same goal: trustworthy finality for the pros, and a fairer playing field for the rest of us.

With that context, let's dive into the core first principles that Paradex has built around, and how each principle translates into concrete features and advantages.

Paradex's signature design innovation is how it handles trade flow. It starts by asking a simple question: what if we made that "last free look" high-speed game mostly irrelevant? Instead of spending engineering effort on who wins the cancel-vs-taker race (a race that inherently rewards speed and hurts retail traders), Paradex tries to make the race itself matter less in the first place. It does this with two complementary mechanisms, Retail Price Improvement (RPI) and Request-for-Quote (RFQ), which fundamentally alter how liquidity is shared and consumed on the exchange.

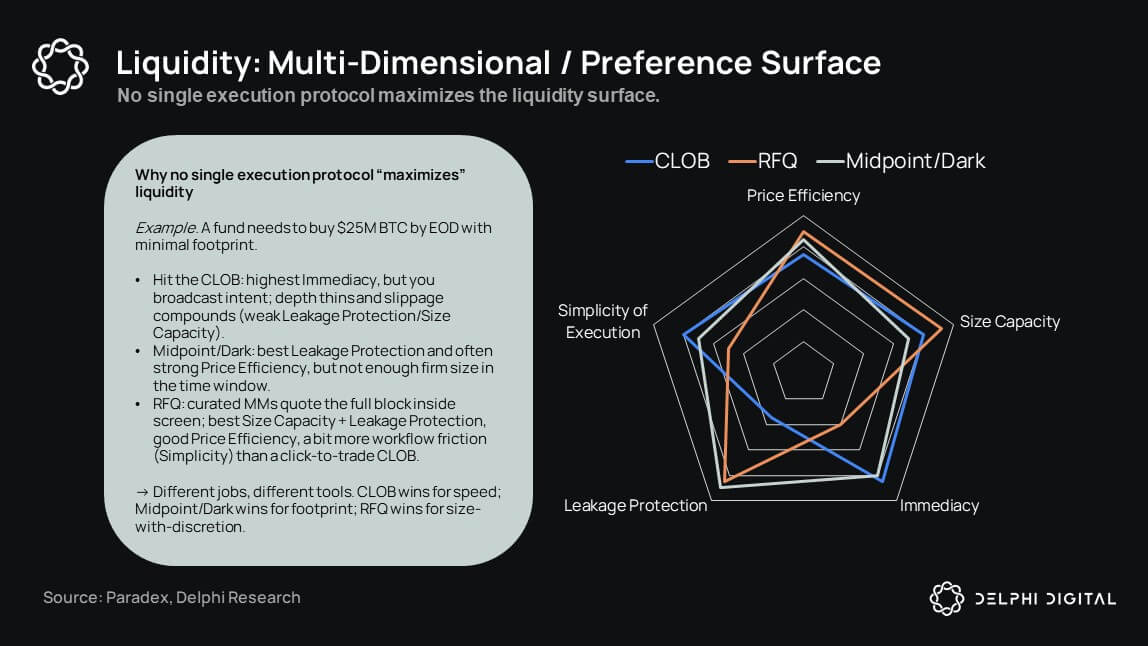

From Anand, CEO of Paradex/Paradigm: "We've always thought of liquidity as an n-dimensional vector in a tradeoff space. This completely changes how you think about building a marketplace. In this world, execution sits on a frontier where CLOBs, RFQs, and dark pools (execution protocols) each optimize for different axes – price, size, immediacy, info-leakage risk, execution complexity. You can slide along this frontier, but you can't max every dimension at once (like the blockchain trilemma). That also means, there is no perfect venue or protocol…….just as there is no perfect blockchain. Only fit-for-purpose protocols and chains. Rational traders choose the microstructure that best matches their objective function and constraints for a given asset, instrument, or strategy."

This idea of sliding along this pareto frontier is what is important as you shift your preferences as a trader.

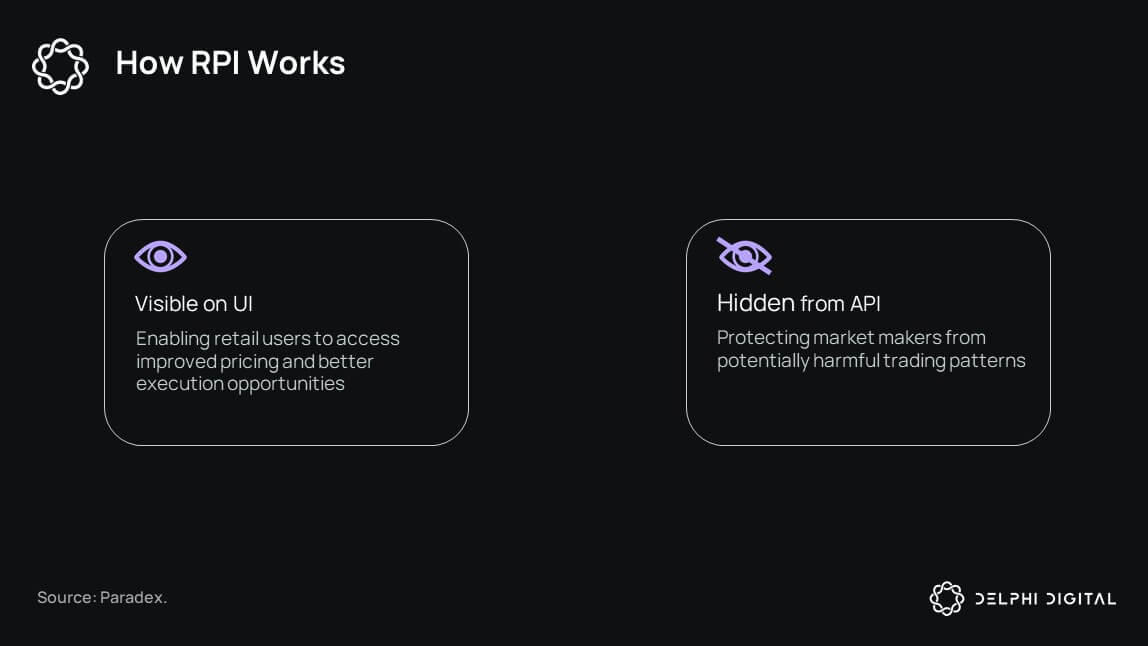

Retail Price Improvement (RPI) is a UI-only price-improvement lane that gives retail traders better prices while insulating market makers from toxic/latency-arb flow. Makers flag their quotes as RPI, making them visible in the app but not via API. These orders are post-only and can only match with non-algorithmic (UI) orders; they never execute against API flow. Practically, this creates two views: an RPI Book (visible only in the UI) and an API Book (visible in both UI and API). UI traders see both; API participants see only the API Book. Because RPI quotes are shielded, makers can post tighter spreads and larger size. Combined with the low friction of zero Taker fees, UI traders naturally interact with top-of-book RPI quotes via simple market orders, delivering better prices, deeper size, and zero fees.

This flow segmentation via RPI allows for a unique business model that is oftentimes overlooked, payment for order flow (PFOF), but is often seen and discussed as zero-fee trading.

Payment for Order Flow is a system where a trading platform (broker or exchange) routes customer orders to specific market makers in exchange for a fee. In simple terms, instead of charging you a commission, the platform gets paid by a third-party market maker for the right to fill your order. This behind-the-scenes payment is what allows some platforms to advertise "free" or zero-fee trading, because someone else is footing the bill for trade execution. (If you've ever wondered how brokerages make money on 0% commission trades, PFOF is usually the answer.)

PFOF enables trading platforms to charge zero taker fees to users while still giving the platform a revenue stream. It creates a sustainable business model where you, the trader, pay nothing to trade, yet the business earns income on every order filled (since a market maker pays for each order). Think of it like a shopping mall with free entry for customers: shoppers roam freely without paying an entrance fee because the stores (analogous to market makers) pay rent to the mall for access to those customers. Similarly, with PFOF the "rent" is paid by market makers to the platform for access to order flow, so traders enjoy fee-free transactions.

Platforms like Robinhood famously pioneered this model. More than 75% of Robinhood's revenue in 2020 came from PFOF (rising to about 81% by early 2021), and the company essentially acknowledged that PFOF is what allows it to offer commission-free trading. In other words, without PFOF, commission-free trading at scale wouldn't be possible for many brokers.

In short, because it's profitable for market makers. Retail traders' orders are often considered "uninformed" flow (not based on proprietary market-moving information) and thus carry less risk to trade against. Market makers covet these retail orders and are willing to pay a small fee for each one to secure a steady stream of this business. They make their money off the bid-ask spread on each trade.

By paying the broker a tiny amount per share (often just fractions of a penny) for the order flow, a market maker gets to fill your order, often at a slightly better price for you, and then pocket the remaining difference in the spread as profit. Market makers pay for retail order flow because those trades pose the least risk and still allow them to profit from small spreads. Meanwhile, you, the user, benefit because the broker can afford to waive your trading fees (since it's earning revenue from the market maker instead). It's a win-win scenario: you trade for free, the market maker earns from the spread, and the platform earns the maker's fee.

By relying on PFOF, Paradex can align incentives in a way that keeps the platform financially healthy without charging users directly. Rather than depend on high taker fees, Paradex will monetize by essentially "selling" the flow of its retail orders to liquidity providers (market makers) who compete for that flow, something made possible only because of flow segmentation via RPI (Retail Price Improvement).

In other words, the RPI program lets Paradex tag and isolate high-quality retail order flow, which the platform can then offer to market makers in return for PFOF revenue. This means the more volume Paradex users trade, the more revenue the platform earns, all while users continue to enjoy zero fees.

This model has already been proven in traditional markets: zero-commission stock brokers generate significant income from PFOF (U.S. brokers collectively earned around $2.5 billion from PFOF in 2020). By making trading free for participants, PFOF encourages higher trading activity and deeper liquidity on the platform, which in turn attracts more market makers willing to pay for that order flow. This is only made possible via RPI and flow segmentation which causes spreads to be tighter than their peers and in some cases better than Binance. "Binance spreads, but with zero fees." The result is a positive feedback loop of liquidity and growth, funded by those who profit most from the trades (professional market makers) rather than by charging casual traders.

Centralized exchange distribution runs on affiliates (KOLs). At scale, the big venues rebate 60–90% of taker fees to top referrers and often sweeten it with token/equity. That lets them lock up the influencers who control user flow. For a smaller venue or a DEX to "outbid" that, you'd have to (a) match or exceed those rev-shares without the volume base, and (b) still fund your own ops/liquidity incentives. It doesn't pencil out. The result is a structural moat: high fees → big KOL kickbacks → captive distribution.

Zero taker fees financed by PFOF is the only credible wedge. Instead of taxing users to fund KOLs, Paradex charges makers a tiny fee for curated, low-toxicity flow (via RPI) and drops taker fees to zero. That does three things at once:

Quick back-of-napkin: Centralized exchanges today: taker fee 6 bps → 80% to KOLs (-4.8 bps) → exchange nets ~1.2 bps; user pays 6 bps + spread. Paradex: taker fee 0 → maker pays ~1.0 bps on curated flow → Paradex nets ~1.0 bps; user pays 0 bps + (often tighter) spread.

This is how you pry users from a KOL-fortified incumbent, make the experience cheaper and the execution as good or better. This only works if your flow is worth paying for. That's the point of RPI/flow segmentation: retail/UI flow is less toxic, so makers pre-commit to quote quality and size and pay a small toll to access it. Any upstart exchange that can't out-compete KOL payouts has to compete on user total cost and execution quality. Execution cost is not just spreads. Execution cost = spread + fees + slippage. PFOF + zero taker fees is the only path I see today for new entrants to disrupt the incumbents. Everything else is just losing a bidding war for influencers or won't scale with users and latency.

Paradex routes value from those who profit most (professional makers) to those you need to win (traders), and the pitch is incredibly simple: Binance-level spreads, zero fees, and often better realized execution.

Paradex is incubated by Paradigm, the institutional liquidity network that trades $1.5B per day in options volume, which is 30% of Deribit, and their request for quote (RFQ) system is on track to be integrated into Paradex later this year (October/November).

RFQs maximize for immediate liquidity, large size and atomic execution of multi-leg trades and are especially important for lower liquidity markets/instruments like options. Instead of slamming a huge market order into the order book (and eating horrendous slippage), a trader – retail or institutional – can privately request quotes from a curated list of liquidity providers. Those providers respond with firm bids/offers, and the trader can choose the best quote to execute, all without ever exposing the order to the public book or tipping their hand. This is exactly how institutions handle large blocks in OTC markets today.

By letting big trades happen in the shadows via RFQ, Paradex prevents those trades from spooking the wider market or getting front-run by algorithms. Again, it's about offering choice of execution modality: if you want to trade big, you don't have to cross your fingers against slippage, you can negotiate price directly with market makers through RFQ and get a firm, private fill.

By introducing flow segmentation through RPI and RFQ, Paradex flips the script on the usual DEX mechanics. It's no longer a single open arena where everyone from a small retail trader to a Jump Trading bot competes under the same rules (rules which end up favoring the Jump bot). Instead, there are two lanes on the same highway that will utilize multiple execution environments. The fast lane (API) is still there for pros and market makers, fast, competitive, open. And there's a slow lane for retail via the UI, where the speedsters simply aren't allowed. If you're a high-frequency trader, you can't even access those RPI orders; you're constrained to the lit book. The slow lane isn't about hiding trades (RPI quotes actually appear in the UI's order book display, sometimes creating a visibly crossed spread inside, they're just invisible to API users), but about controlling who can interact with whom.

The result is profound: Makers don't need a free cancel option to protect themselves from toxic flow in the slow lane, because the toxic flow never enters that lane to begin with. They can tighten quotes and keep them firm. The game of "quote → get pinged → yank → repost" largely disappears for retail flow, because makers aren't constantly trying to avoid being picked off, the retail flow is, by construction, non-pickoff-able. This greatly reduces cancel spam and the flickering liquidity issue. In effect, Paradex's approach pre-discriminates between flow types: it offers pre-trade segmentation (RPI/RFQ) instead of post-trade band-aids (cancel-priority). If the goal is fair prices for humans and sustainable economics for liquidity providers, this first-principles approach makes a ton of sense. Retail gets inside-spread fills; makers face less adverse selection; and the system doesn't have to bleed edge to latency arms races.

I'd go as far as to pose this challenge: If an exchange can selectively improve prices for real human traders and even execute multi-leg packages atomically, what real edge does cancel-priority still buy you? I would argue very little. The usual answer is "speed", but when you're playing on-chain, absolute speed is capped by block times anyway, and Paradex would rather use that budget to enforce fairness than to allow TPS wars which could become obsolete as complexity of transaction will greatly affect latency moving forward.

Now, I'm aware enough (and battle-scarred enough) to note two caveats: (1) The market might not care. It's possible that traders, even retail ones, are indifferent to these microstructure nuances, albeit it's hard to be indifferent to zero fees. If Hyperliquid or a Solana-based exchange feels "fast and liquid" enough, users might not ask questions about how or why their fills are the way they are. Paradex's superior design could be an academic win but a market adoption loss if users simply chase whatever has volume and hype. (2) I could be wrong that this model scales better. Perhaps cancel-priority plus brute-force speed is the optimal solution and will always attract the most volume, especially from quant traders who generate a lot of flow. These are fair points, technology and market structure alone don't guarantee success in the market. But as someone who's spent years in the weeds of trading, I strongly believe Paradex's approach addresses the root problems rather than the symptoms. It's a longer-term bet on structural advantage over speed-based advantage.

At minimum, Paradex is pushing the conversation forward. DeFi shouldn't just be about copying TradFi under worse conditions; it should be about improving on TradFi using crypto's superpowers (and avoiding its traps). On that front, RPI/RFQ vs. cancel-priority is the clearest fork in the road, in my mind at least. Paradex is firmly planting its flag on the side of RPI/RFQ, and I suspect a year from now many others will follow that lead if it proves out. Ultimately, I see Binance watching from afar until they copy/paste RPI/RFQ and use it on their platform.

There's another fundamental mismatch when porting traditional markets to DeFi: the on-chain world is completely transparent by default. That might sound great for "trustlessness," but when it comes to trading, too much transparency is a bug, not a feature. In TradFi, if a fund wants to sell 50,000 shares, they don't display that entire order on an exchange for everyone to see. Yes, we will see it in their 13F a quarter later, but that is besides the point because we don't see their trade live. Instead, they work the order discreetly or use a dark pool – a private exchange – exactly to avoid telegraphing their intent and getting front-run. Dark pools and block trading mechanisms exist because big players simply won't trade if everyone can see and exploit their hand. If we expect serious institutions (or even savvy whales) to trade on-chain, we need to offer them ways to move size without painting a target on their backs.

Frankly, you can't scale finance without privacy, and Wall Street demands it. Even aside from institutions, many crypto traders also value not broadcasting their positions to the world in real time, especially for large or strategic positions. You can have your own opinion about the ethos of transparency (witness the debates around things like James Wyden's proposal for on-chain surveillance, or the Tornado Cash saga), but the bottom line is clear: if we want the big money to come on-chain, we must provide privacy and discretion similar to what exists in traditional markets. Otherwise, large players will stay away or use only heavily intermediated channels.

Paradex recognizes this and has built privacy into its protocol at multiple levels:

Hidden Retail Orders and RFQ

As mentioned in the RPI discussion, retail orders on Paradex's UI are effectively only visible to other retail users. These orders are not visible to anyone scraping the network; only the Paradex matching engine and its market-making partners see them. This means if you place a small order, no external bot can detect it and frontrun you in the mempool. Contrast this with a typical DEX on Ethereum L1, where a user's transaction (order) sits in the public mempool for 12+ seconds, giving arbitrage bots ample time to pounce. Paradex's design (with its off-chain matching and private order submission) avoids that entirely. In effect, retail gets a mini dark pool, their orders won't show up publicly until after execution, preventing them from being preyed upon by faster actors.

Encrypted Positions On-Chain

Paradex is rolling out on-chain privacy for position data. Today, if you open a large position on most on-chain protocols, anyone can see it on the blockchain and potentially infer your strategy, copy you, squeeze you, or avoid trading against you. Paradex plans to encrypt position state on-chain such that only you (and the exchange's risk engine) know your current positions. This will happen in phases (as zero-knowledge tech and infrastructure permit), but it's a core part of their roadmap. In practical terms, this means if you have, say, a huge long position, others won't be able to scan the chain and adjust their trading or liquidations to exploit that. Your position data remains private, even though the system as a whole still proves validity via zk-proofs. It's a bit like having the benefits of a dark pool for after you trade, not just during the trade.

Off-Chain Matching & Mempool Protection

From day one, Paradex's matching occurs off-chain, and trades are settled on-chain only after the fact (bundled in zk-proofs). This ensures there's no public mempool competition for your order. When you hit buy or sell, you're not broadcasting that intent to miners or validators who might reorder transactions against you. The trade executes in Paradex's off-chain engine (which is run by the decentralized sequencer), and then the outcome is committed on-chain in a batch. This gives deterministic execution (more on that in the next principle) and also means no on-chain front-running is possible. In short, Paradex's current architecture already prevents the typical DeFi issues of sandwich attacks or MEV extraction on trades, because those opportunities never appear in a public mempool.

Big players can work large orders via RFQ. Small players don't have to worry that someone is monitoring their every move on-chain or that a faster bot will intercept their trade. Transparency is preserved where it's actually needed, for verification (all trades ultimately go through the zk-proof and can be verified for correctness), but it's removed where it causes harm, i.e. in the real-time market data that others could exploit.

The Nasdaq and NYSE have long provided ways for traders to not broadcast their full hand (iceberg orders, dark pools, upstairs block trades, etc.), precisely to encourage big liquidity to come in. Paradex providing similar capabilities on-chain is not only a selling point to institutions but also a protective feature for retail (who often are the ones exploited by lack of privacy). In crypto, we've seen debates flare up (e.g., the James Wyden saga about on-chain dark pools). But, I suspect privacy will become a standard expectation in a few years for any serious on-chain trading venue.

Speed and fairness are vital, but so is certainty. If you're a professional trader hedging millions in basis trades or options strategies, the last thing you want is a trade that you thought was final getting undone hours or days later. This is a non-negotiable: finality must be deterministic and immediate. In the centralized exchange world, once a trade is confirmed, you trust it's not going to be retroactively busted (barring extreme events).

Paradex recognized early that it needed deterministic, immediate finality on every trade. This drove a crucial decision: build on zk-rollup technology rather than optimistic rollups or other L1s. In a zk-rollup, every batch of transactions comes with a cryptographic validity proof that the new state is correct; once Ethereum verifies that proof, the state update is final. There is no challenge period or re-org risk beyond Ethereum's own finality. In other words, finality on a zk-rollup is as strong as math – once the proof is accepted, your trade is irrevocably settled. This is exactly what a trading venue needs.

Paradex Exchange is built on the Paradex Chain, a CairoVM-powered, Ethereum-settled L2, purpose-built for high-throughput derivatives. It shares state with Paradex Exchange, enabling a fully composable, high-throughput execution environment where on-chain applications can seamlessly interact with the deep liquidity infrastructure they've built over the past year. Some of you likely know that CairoVM also powers Starknet and STRK based scaling, which has been leveraged by other platforms like dYdX in the past.

CairoVM is a purpose-built virtual machine for STARK-based validity proofs, enabling high-throughput ZK rollups on Ethereum. Designed from first principles, it isn't constrained by the EVM architectures. Smart contracts are written in Cairo, a Rust-inspired language that compiles to proof-efficient code for fast verification. STRK powered rollups are (a) post-quantum secure and don't require a trusted setup (pioneered by Starkware, a leader in production ZK systems) and (b) more efficient over SNARK based verification. Vitalik has commented several times on the superiority of STRK based scaling.

This STRK powered stack gives Paradex an unprecedented scaling advantage. It unlocks extremely complex and computationally heavy portfolio-margin and multi-collateral computation on large portfolios without the need to create separate margin pools for spot, perps, and options. This unlocks a unified margin experience across spot, perps and options without the need to transfer collateral between pools and ensuring state composability with borrow/lend markets.

STRK powered rollups give Paradex the best of Ethereum's security (every proof is settled on Ethereum L1) while having full control over the execution environment (their own sequencer, custom matching logic, etc.). They often describe it as having Ethereum be the high court (the source of truth) and the Paradex chain be the day-to-day government for trading. Ethereum (via the zk-proof verification) is the impartial risk manager enforcing finality and correctness, while Paradex's own chain is the high-speed execution engine that can evolve rapidly, add features, and optimize for trading.

Now, one might ask: why not just use a high-speed monolithic chain like Solana, or a generalized L2 like Arbitrum or Optimism? Because an exchange can't afford to blur Church and State. You want the State (the final arbiter of truth) to be neutral, boring, and unchangeable; and you want the Church (the domain of policy and experience) to move fast, experiment, and optimize for growth. Paradex splits those roles cleanly:

State = Ethereum + STARK validity proofs (the "constitutional court") — This layer enforces the law: deterministic finality, provable correctness, solvency. It's the risk manager, hard limits, no "vibes", no exceptions, no seven-day fraud windows.

Church = Paradex app-chain execution (the "government" you can change) — This layer sets day-to-day policy: matching logic, RPI/RFQ routing, maker access lists, risk haircuts, cancel rules, UI/UX. It's the portfolio manager, free to optimize, innovate, and iterate to seek better P&L for users.

When a single chain tries to be both Church and State, you get conflicts of interest: fee-market spikes, mempool games, and global scheduler decisions that can randomly rewrite your microstructure mid-trade. By separating the risk manager from the portfolio manager, Paradex gets the best of both worlds: the risk core is mathematically rigid and independently verifiable on Ethereum, while the execution surface can evolve quickly without endangering finality or solvency guarantees.

To put it even simpler: a trader and risk manager cannot be the same person, not because a trader can't do a risk manager's job and vice versa, but because there is an inherent conflict of interest. Too much of one comes at the cost of the other.

Therefore, why not just use Solana or a generalized L2? Because you can't be both the Church and State at once. Settlement/security should minimize variance; execution should maximize growth. Paradex wants the trader's stack, full control over microstructure, while Ethereum acts as the impartial court of law. That's why they chose a bespoke zk app-chain on Starknet: tune matching logic, embed RPI and custom risk/PM at the protocol layer, and avoid other networks' congestion/governance drift, while settling to Ethereum for finality. On trading desks, risk managers literally sit on a different floor from portfolio managers, by design. Risk enforces limits; the trader seeks edge. Asking one chain to do both yields the worst of each.

Additionally, frankly, Paradex didn't need to piggyback on another ecosystem's user base or liquidity, Paradex knew it could bootstrap distribution by itself, given that it sprang out of Paradigm (a network of 3,000+ institutional traders doing ~$1B daily volume OTC). They aren't a scrappy project begging for users, they have a pipeline of allocators waiting to onboard if the tech works as promised. However, I would be remiss if I did not note that I think Paradex underallocated resources to distribution. I argue that Paradex is better than Hyperliquid and better than Binance, but if this is the case then why has no one heard of them? Answer = the lack of distribution. Think of good distribution as "shots on goal." If you have good distribution then you have more "shots on goals", therefore, higher probability of your company being a success. Anand and co. realize they have not allocated enough time or resources to distribution and are actively working on increasing distribution now that their product offering is better than their peers. I am optimistic that daily active users (DAUs) will 4-5x over the next 6-12 months as marketing ramps up.

Thus far I've focused on trading mechanics, spreads, cancels, etc. But Paradex isn't just tweaking how the order book works, they are building an all-in-one trading and investment platform. The vision is closer to a "prime broker" than a single-purpose exchange. Under one roof, and one unified account (real), you'll be able to trade spot, perpetual futures, perpetual option (I like to view as 0DTE options in crypto), and (soon) options, and also earn yield or borrow, all cross-collateralized against one portfolio. This addresses a huge pain point in both CeFi and DeFi: fragmented accounts and siloed capital. On FTX or Binance, for instance, you had separate margin pools for different products (spot vs USD perps vs coin-margined perps), which was capital-inefficient and a headache. Many DeFi platforms are one-trick ponies (only perps, only spot, etc.) and if you want to do something like borrow against your LP tokens or hedge an options position, you're moving assets all over the place. Paradex said "enough" and built everything on one ledger.

I want to break down some of the innovative product features and integrations Paradex offers thanks to this unified design:

Universal Cross-Margin & Portfolio Margin

This will be one of the biggest unlocks and most difficult to copy by consensus chains given complexity of transactions and cost. Paradex will soon offer true portfolio margining across multiple asset classes (spot, perps, options, vaults, etc.). All your assets in your account contribute to a single collateral pool. Gains on one position can offset losses on another in real time, reducing your overall margin requirement. For example, if you're long 1 BTC in the spot market and short 1 BTC in a perp, those positions largely hedge each other, Paradex's engine recognizes that and doesn't make you post full margin on both legs (something a typical exchange might require if the products are siloed). This is a huge unlock: even many major CeFi venues don't offer true cross-product portfolio margin (or only offer it to very large clients). On Paradex, it's available to all by default. This means users can trade larger sizes with the same capital, or conversely, need to keep less idle margin for a given strategy. This should equate to roughly 80-90% less margin required for a basis trade. From a competitive standpoint, this attracts sophisticated traders who care about capital efficiency. It enables strategies like basis trades (spot vs perp arbitrage) or multi-legged option spreads to be done much more efficiently on one platform. Implementing portfolio margin is notoriously complex (risk models, default fund, etc.), but Paradex's team has the pedigree (they built Paradigm's systems and many came from trading backgrounds) and by controlling their own chain, they baked this functionality in at the protocol level.

Perpetual Options

One of the more novel products Paradex has launched is perpetual options, essentially options with no expiry date, but I think users will use them more closely to the way they do 0DTE options. However, please don't forget that options are incredibly powerful hedging instruments. Just like perpetual futures (perps) removed the expiration/rollover issue for futures, a perpetual option charges a continuous funding fee to represent time decay (theta) instead of having a fixed expiration. The idea is powerful: crypto traders love options (witness the explosion of weekly and even daily options in TradFi – e.g. the 0DTE craze). A perpetual option would let traders hold an options position indefinitely, adjusting their funding paid/received, without worrying about rolling over contracts every week or month. This could open the door to much higher options participation on-chain, because managing expiries is one of the pain points that keeps people away. It's a complex product to engineer (pricing, funding mechanisms, risk management for infinite duration), but if anyone can crack it, it's Paradex's team (remember, Paradigm facilitates ~30-35% of Deribit options volume, so they know this domain intimately). Paradex plans to offer regular dated options as well, meaning it could become the first on-chain exchange that truly challenges Deribit's monopoly on crypto options liquidity.

Unified Collateral and Synthetic USD (XUSD; similar business model to Ethena)

You will soon be able to deposit a range of assets (ETH, USDC, BTC, etc.) and all count toward your margin. Paradex will automatically convert assets to an internal accounting unit called XUSD for margining purposes. XUSD is basically a synthetic stablecoin that represents your dollar-equivalent balance on the platform. If you deposit, say, 1 ETH, the system will credit you some amount of XUSD (valuing the ETH at market price) which you can then use to trade any market. This means you don't have to manually swap into USDC or whatever the quoted currency is for each trade, any asset can be collateral for any trade. The system will handle FX conversions in the back-end. The cool part is that XUSD balances earn yield in the background. Paradex can take the actual assets (like that 1 ETH you deposited) and, while it sits as collateral, deploy it into safe yield strategies (like lending on Aave, Morpho, or another money market, or in the future via its own lending pools). The yield generated can be passed back to you or shared with the protocol. This is similar to what some prime brokers do with client cash (sweep it into money market funds), but here it's transparent and on-chain. It also hints at another business line: Paradex can earn interest on user deposits by deploying collateral, effectively acting like a bank in addition to an exchange.

Integrated Money Markets (Borrow/Lend)

Because Paradex's platform has a concept of universal collateral and a native ledger, it can allow borrowing and lending seamlessly against your trading positions. For example, you could hold a bunch of BTC as collateral and borrow USDC against it within the same account to then trade or withdraw, without moving assets to a separate lending protocol. Or vice versa: you could lend out your idle stablecoins to earn interest, while still using them as collateral for your trades (effectively rehypothecating within safe limits). This is akin to having Aave/Morpho built into the exchange. In practice, Paradex could either integrate a proven money market protocol or run its own simple one, but the key is the synchronous composability, the lending and trading occur on the same ledger, so you don't have weird timing or bridge risk between platforms. For the user, it's just one platform: deposit assets, and then you can either trade with them or lend them out or both, all tracked by the same risk engine. It's easy to imagine, for instance, borrowing against the equity in your Perp positions (something you absolutely cannot do on separate platforms) or short-selling an asset by borrowing it and selling, all in one place. This blurred line between exchange and bank is a frontier that Paradex is exploring. It makes the platform more capital-efficient and gives users more ways to put their money to work without leaving the ecosystem.

Tokenized Asset Management (Vaults; Similar to Blackrock's Business Model)

Not everyone is an active trader; many users just want to earn yield or invest in strategies passively. Paradex offers Vaults, essentially on-chain funds or strategy containers, that users can deposit into to get yield from certain strategies (market making, arbitrage, trend following, etc.). These vaults are like having a BlackRock or a hedge fund within the exchange. Importantly, vaults on Paradex are first-class citizens: a vault can trade on the exchange just like a user. For example, a market-making vault could place orders on Paradex and earn trading fees; a yield farming vault could use Paradex's money markets to lever up; etc. Users who deposit get a token (representing their share of the vault) and those vault tokens can themselves be used as collateral on Paradex. Imagine you put USDC into a BTC trend-following vault; you get back VAULT tokens. You could then use those VAULT tokens as margin to trade other products, or even borrow against them. It's a glimpse of a world where your entire portfolio lives on one platform, and you can do complex things like "earn yield in a vault while that vault token collateralizes a leveraged bet elsewhere." From a user perspective, it's extremely powerful (though one will need to manage risk). From a platform perspective, it increases stickiness: if someone has trading positions and vault investments and maybe a loan all on Paradex, they are deeply ingrained and less likely to leave.

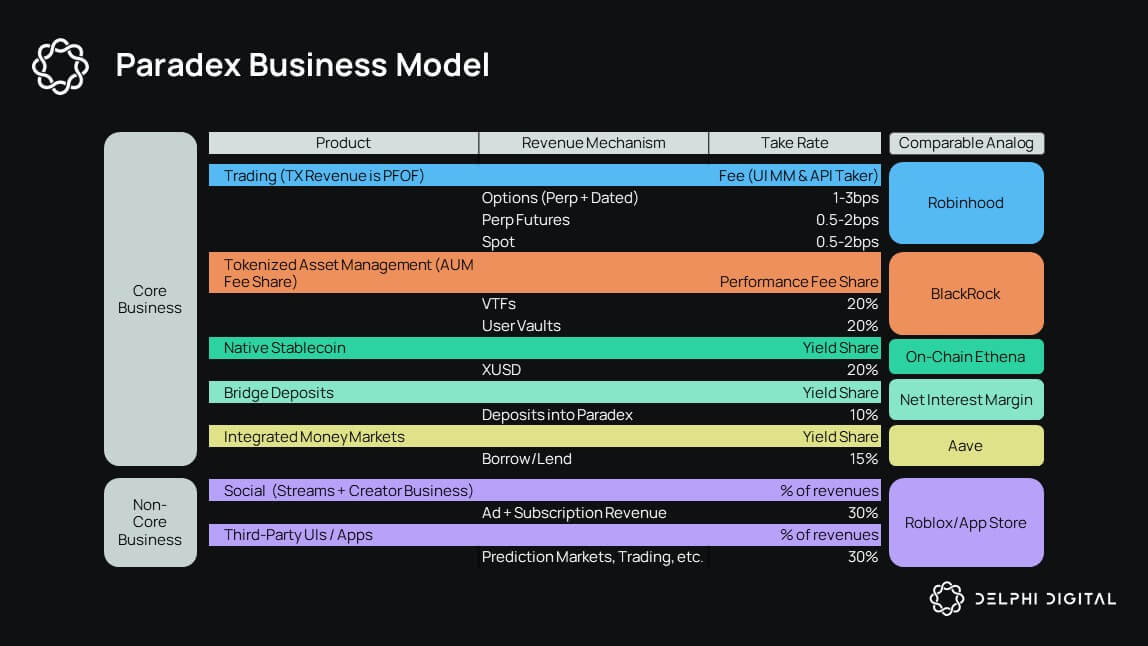

To summarize these features more succinctly, Paradex is combining functionalities that in traditional finance (or even current DeFi) are handled by separate entities. Here you get it all in one place: Exchange/Brokerage (trade spot, perps, options with zero fees and tight spreads), Custody & Prime Brokerage (use all your assets under one account with portfolio-wide risk management), Banking/Lending (earn interest on idle funds, or borrow against your portfolio), Asset Management (invest in structured products or vaults for yield), and Dark Pool/OTC (execute large trades discreetly via RFQ or hidden orders without moving to another venue).

This breadth not only creates multiple revenue streams for Paradex (trading fees, net interest margin, vault fees, etc.) but also makes the platform extremely sticky. A user who only trades perps might hop around platforms chasing the best liquidity or incentives. But a user who has an integrated setup on Paradex, maybe running a basis trade that uses spot, perps, borrowing, and an options hedge all together, will find it very hard to replicate that elsewhere without losing efficiency.

Another angle to note, because Paradex is essentially an Ethereum-aligned rollup, it can potentially allow other dApps or smart contracts to deploy on the same chain. Paradex has floated the idea of third-party "apps" or extensions in its ecosystem, think of community-built streaming services, a marketplace for agents, games, analytic tools, or even entirely new financial products that plug into Paradex's liquidity and user base. They even liken this to turning the exchange into an app store (or Roblox-like platform) where developers can build on top of the Paradex infrastructure and user pool.

In essence, Paradex rolls the business models of several financial institutions into one. It's simultaneously: a retail broker (zero-commission trading), a market maker aggregator (earning PFOF from liquidity providers), a bank (earning interest on deposits and lending), an asset manager (offering vault products and taking a performance fee cut), and a mini app-store (taking a platform fee from third-party apps built on it). All of those value streams ultimately accrue to the Paradex ecosystem (and its token, which we'll discuss next). This is a first in the crypto exchange landscape, most others focus on one slice (just trading fees, or just AMM LP fees, etc.).

To drive this point home, consider the analogies: Paradex is positioning itself as on-chain Robinhood + Blackrock + Aave + Roblox. It's a platform play rather than just an exchange. When evaluating Paradex's potential, this breadth means you're looking at multiple addressable markets, not just exchange trading fees. A successful Paradex could capture revenues similar to a brokerage, a bank, an asset manager, and a DeFi protocol combined.

It's no secret that the 2023-2024 meta for exchange tokens (and many other crypto tokens) has been broken. Low circulating floats, sky-high fully diluted valuations (FDV), and vague promises of future utility have been the norm. Early insiders get tokens at fractions of a penny; retail sees the token listed at a $5B-$10B FDV on day one and effectively becomes exit liquidity for those insiders over time. Hundreds of thousands (if not millions) tokens launched in 2024, most went down-only after listing, and it's not hard to see why: all the upside was captured in private rounds, and all the sell pressure comes once it's public. This model has burned retail and eroded trust ("another high FDV scam token" is a common refrain), ironically driving traders back into meme coins where at least everything is in circulation and the game is transparent.

Paradex is taking a page from web2 growth playbooks and some recent successes (we've seen community-centric launches do well) to design $DIME, the Paradex token, to be as fair and growth-oriented as possible. While details are still in progress, here's the broad strokes of the approach:

Deep Insider Alignment

Many insiders (team and some contributors) are on long vesting schedules (4 years) with performance milestones. This is almost unheard of in tokens, typically, insiders just have time-based cliffs. Paradex is saying, for example, the team's tokens might not unlock unless the platform hits $X revenue or $Y FDV. This is essentially what MetaDAO founders are doing as well with a convex payout structure. They're locking in that the team only wins if the community wins. It's an answer to the pervasive fear that insiders will dump on the first pump. This also creates a culture of building for long-term value, not just hyping the token for a quick flip. (Notably, Paradex even adjusted some early investor allocations to be performance-based, showing they walk the talk on this alignment.) This type of convexity based payout is more akin to Silicon Valley. This is something that has been left behind by crypto founders that is now, hopefully, being readopted and we will slowly stop seeing companies become unicorns and they slowly die.

Real Utility & Value Accrual

$DIME will, of course, confer governance rights eventually (holders can vote on fee parameters, new features, etc.), but beyond that it has direct economic ties to the platform. Paradex is committing to channel a significant portion of the protocol's revenues back to $DIME holders. The exact mechanism will likely start with buy-and-burn using protocol fees. This means as the exchange generates more revenue, the token should capture that value, similar to how stocks benefit from share buybacks or dividends. Initially, a buyback-and-burn approach is simplest (a transparent way to return value without regulatory headache of explicit dividends). I believe over time, intelligent buybacks will be limit orders and not TWAP market orders dominating the orderbook. In the short term, I think we should expect "90% of revenues will be going to buybacks" optics at play. The key is: $DIME won't be just a pointless governance token; it's designed to be a claim on the success of the network.

Platform Fee Model (Paradex as an App Store)

Remember those third-party apps and vaults that can plug into Paradex? Paradex should and will take a platform fee from any such activity. This is analogous to Apple's App Store 30% cut or Roblox's Robux economy. For example, if someone builds a portfolio management bot on Paradex and charges users a 1% fee, a portion of that (say 0.3%) could automatically be routed to Paradex's treasury (and thus to token holders). This ensures that as the ecosystem around Paradex grows, $DIME holders benefit from all economic activity on the chain, not just the core trading fees. Hyperliquid has great fee-to-buyback design for its own trading fees, but when third-party projects build on Hyperliquid (e.g. Liminal), those projects aren't obligated to share revenue with $HYPE holders. Some do so voluntarily (buying HYPE as a thank-you), but it's not guaranteed. Paradex will make it programmatic, if you build on Paradex and tap its liquidity, the protocol will bake in a revenue share. This could become a significant source of value if Paradex's platform spawns many successful apps.

To appreciate the potential here, consider the revenue streams Paradex could be capturing:

(1) Trading (PFOF) Revenue — Every time a retail taker trade is filled, a market maker pays a tiny fee.

(2) Net Interest on Deposits — If users deposit assets which sit idly or as collateral, Paradex can deploy those into lending protocols to earn interest.

(3) Borrowing/Lending Spread — If Paradex directly facilitates borrowing, the platform could take a cut of the interest as the facilitator.

(4) Vault Performance/Management Fees — If vault strategies are offered, Paradex could take a performance fee or a small management fee.

(5) Stablecoin Float Revenue — Paradex's synthetic USD (XUSD) could generate revenue if the underlying collateral is earning yield.

(6) Third-Party App Fees (Roblox/App Store) — Any external app or partnership that runs on Paradex's chain can be coded to share revenue with the platform.

In short, Paradex could end up with 5+ distinct revenue streams, all feeding the token.

Now, about avoiding the "low float, high FDV" trap: Paradex is likely to do an initial distribution that actually gets a meaningful amount of tokens into the hands of the community (possibly via some retro airdrop or trade mining for early users, etc.), without pricing the FDV at some astronomical level. They've seen how projects that launch at $5B FDV with only 2% in circulation tend to bleed out as vesting releases hit. Instead, Paradex might aim for a modest initial valuation (say a few hundred million to one billion, just as an example) that leaves room for organic appreciation as the platform proves itself.

One more important aspect: Intelligent Buyback Mechanism. Many projects simply say "we'll use X% of fees to buy our token on the market and burn it." Simple, but not optimal. Why? Because it's mechanically inefficient and reflexive in the wrong way. It is -EV. Paradex's community/treasury could instead take a smarter approach. For instance, instead of eating into the order book (which can create volatility and slippage), Paradex can place algorithmic limit orders to accumulate $DIME over time (acting as a buy-wall that supports the "floor price" at team deemed attractive entry points). It could also vary the buyback intensity based on market conditions – e.g. buy more aggressively when price is low (more tokens retired per dollar of revenue) and hold fire when price is high (conserving funds) and focus on growing other business lines. This would prevent the common issue of projects buying a lot of tokens at tops and then having no ammo during dips.

While specifics will be ironed out via governance, it's clear from the team's communication that they want $DIME to mirror equity in many respects – aligned incentives, performance-based unlocks, and value tied to fundamentals (revenues). This is part of a larger industry trend to treat tokens less like meme coins and more like actual stocks.

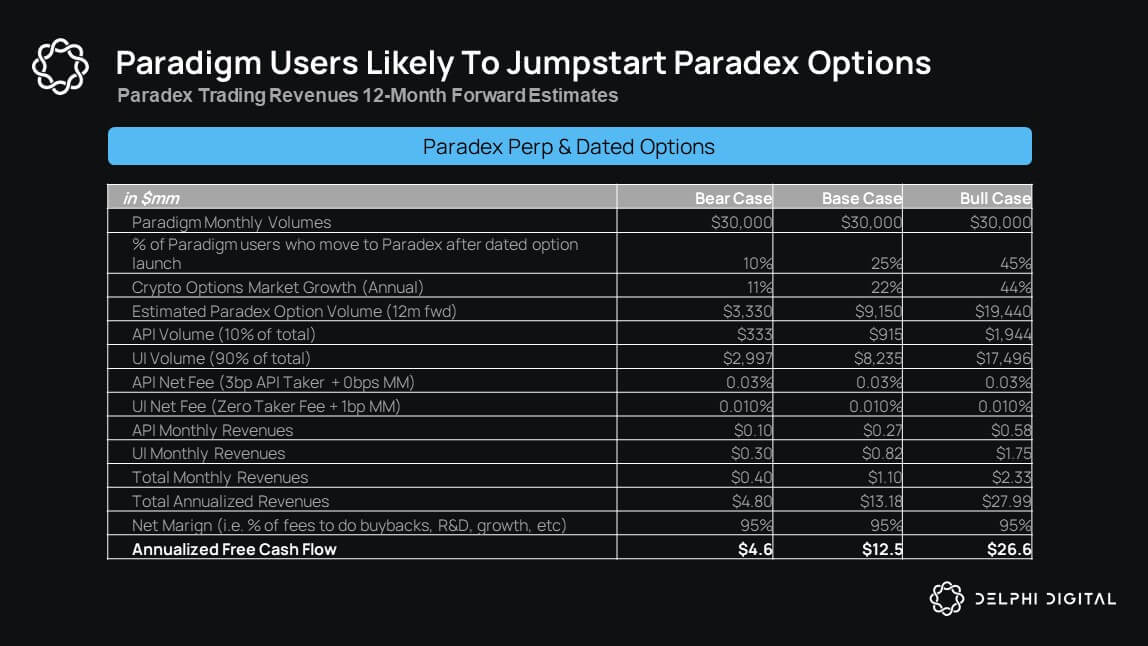

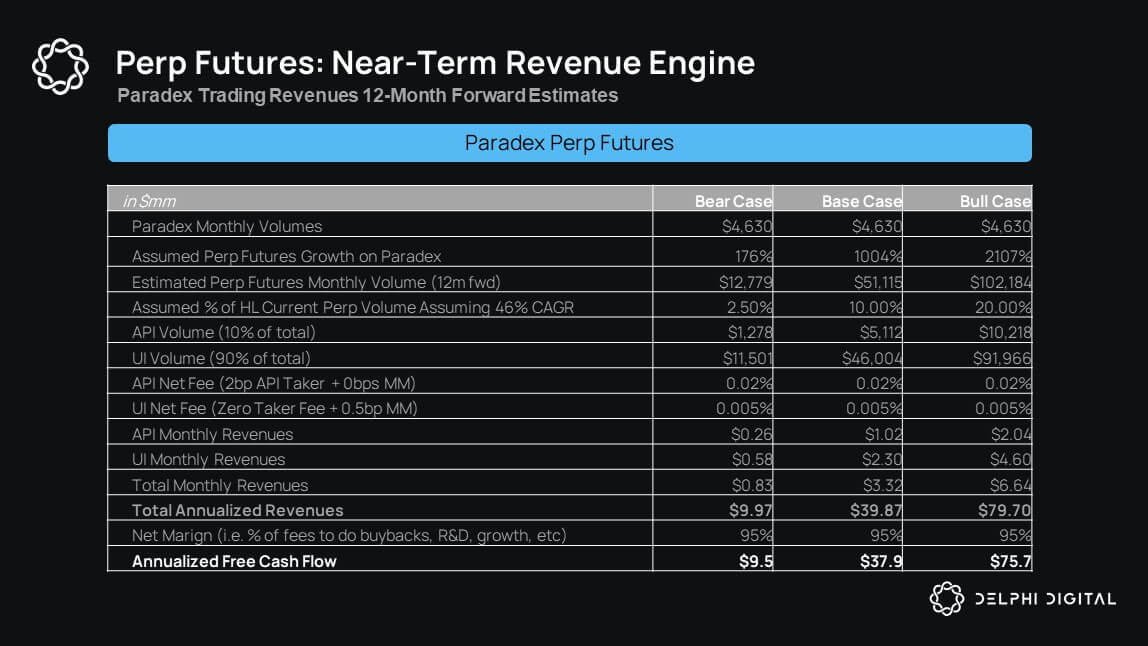

Let's put some numbers to this. Paradigm (the OTC network Paradex originated from) facilitates around $35 billion in crypto options volume per month. Much of that is institutions trading complex products through block trades. Paradex, once it offers the full range of perps and dated options, stands to capture a slice of that massive pie by bringing those flows on-chain. Even a 10-20% migration of Paradigm's volume to Paradex over time would mean billions in monthly volume, which, with even a bp fee, is significant revenue. And that's just one vertical (options). Add perpetual swaps, add spot, add whatever new products can be built thanks to portfolio margin (perpetual options, structured vaults, etc.), and you have multiple robust revenue streams.

While Paradex does have many lines of revenue, over the next 12-months, I have a hard time seeing any business line outside of trading gaining huge traction and being a large driver of revenue. Over the coming 12-36 months I believe this changes and in some scenarios I think we could see a more even split between trading, asset management, and the Roblox like business line. However, I will focus my assumption on the next 12-months as I believe that to be more intellectually honest.

I use Adjusted Market Cap (AMC) as "Price" (P) in a P/FCF setup. Free cash flow (FCF) is net margin × revenue — the dollars available for buybacks, R&D, marketing/distribution, etc.

For all volume data, I assume, at least for now, that the vast majority of flow is coming from the UI (90%) and not the API (10%). Why does this matter? Because the net fees on the UI, are generally speaking, a lot cheaper which will skew revenues lower than what they might be if we see more API users. However, given that the exchange is still relatively small I believe this to be a fair/conservative assumption.

Line item assumptions:

I assume, for my base case, that Paradex will consume 25% of Paradigms dated option volume once dated options are live on Paradex. I also assume crypto's option market will grow 22% over the next 12 months, which I believe to be very conservative as it is only a 2x growth rate over that of equities.

Given the convex nature of options, despite minimal traction thus far, I do believe perp options will see exponential growth as retail views these perp options as 0DTE options and institutions use them for hedging, which could lead to Paradex's options market driving revenues. However, this is not my base case today.

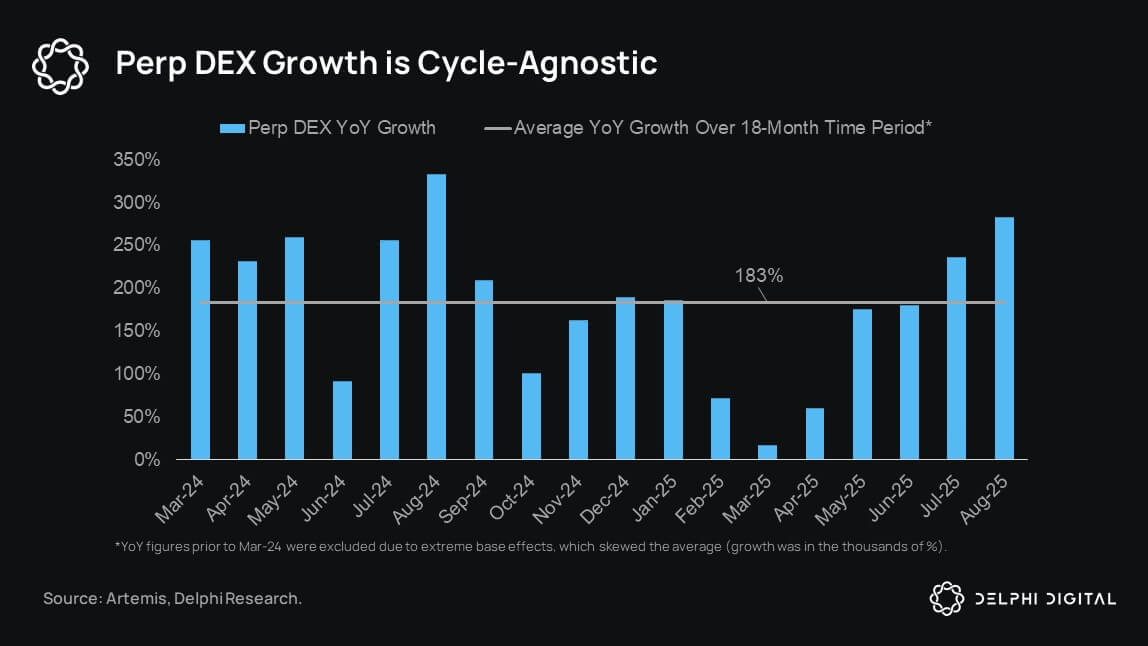

To start off I assume a ~46% growth rate to Hyperliquid's volume which is a ~75% discount to the trailing 18-month YoY growth rate for the entire decentralized perp market. I then use my forecasted volumes to back into the market share I believe Paradex will take over the next 12-months.

Given these assumptions, Paradex's perpetual futures market, I see as the largest contributor to revenues over the next 12-months.

However, it would not surprise me if we see growing interest in their perp options product as it functions similarly to a 0DTE option.

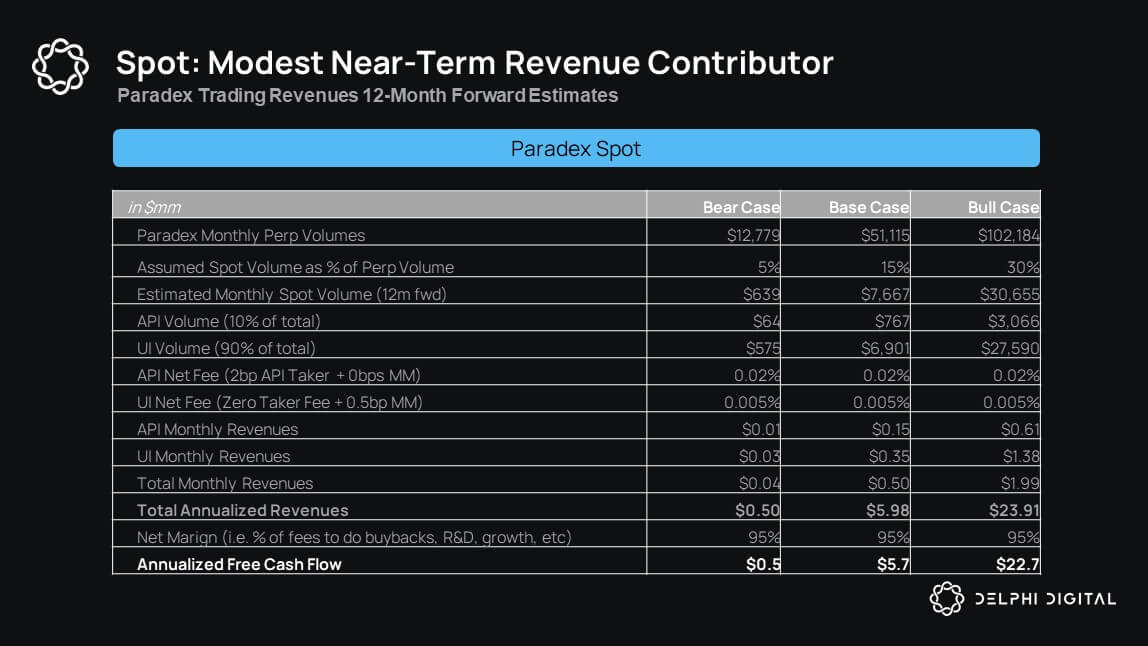

Historically, Binance and other centralized exchanges have averaged a 30% ratio between spot and perpetuals. However, this has not been the case for decentralized exchanges with perpetual offerings. Therefore, a more conservative 15% ratio is my base case assumption of the next 12-months as Paradex rolls out spot markets in the near future.

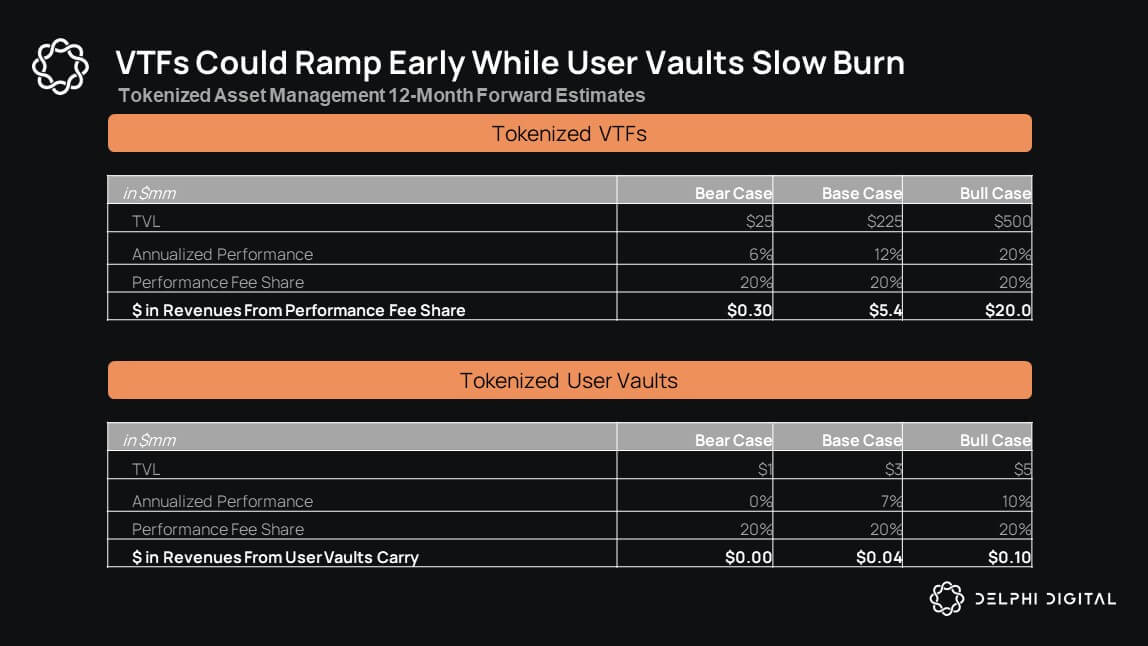

Outside of the Gigavault, I don't model meaningful Year-1 revenue here; I expect contribution to become meaningful over 12-36 months.

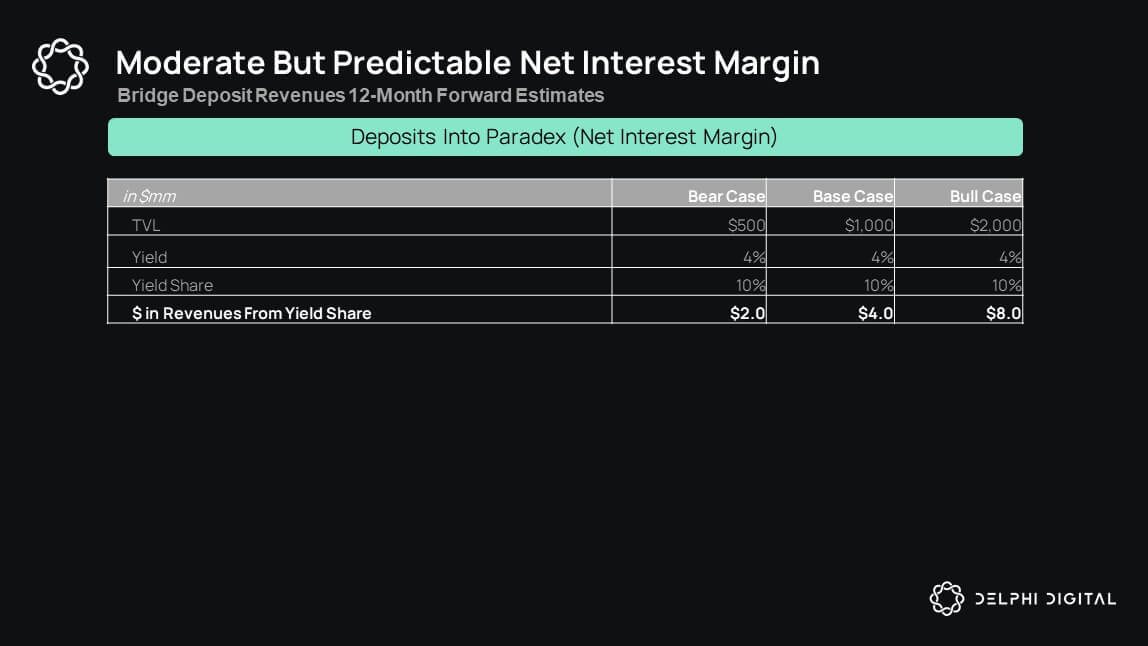

There's real appetite for exchange-native stables. It has become increasingly obvious that perpetual exchanges will launch their own native stablecoin. Once launched, I expect immediate, but modest contribution that ramps with platform growth and provides steady FCF.

Assets locked in the bridge earn a conservative ~4% (treasury yield vs. Aave/Morpho), reflecting a risk-aware posture from the team.

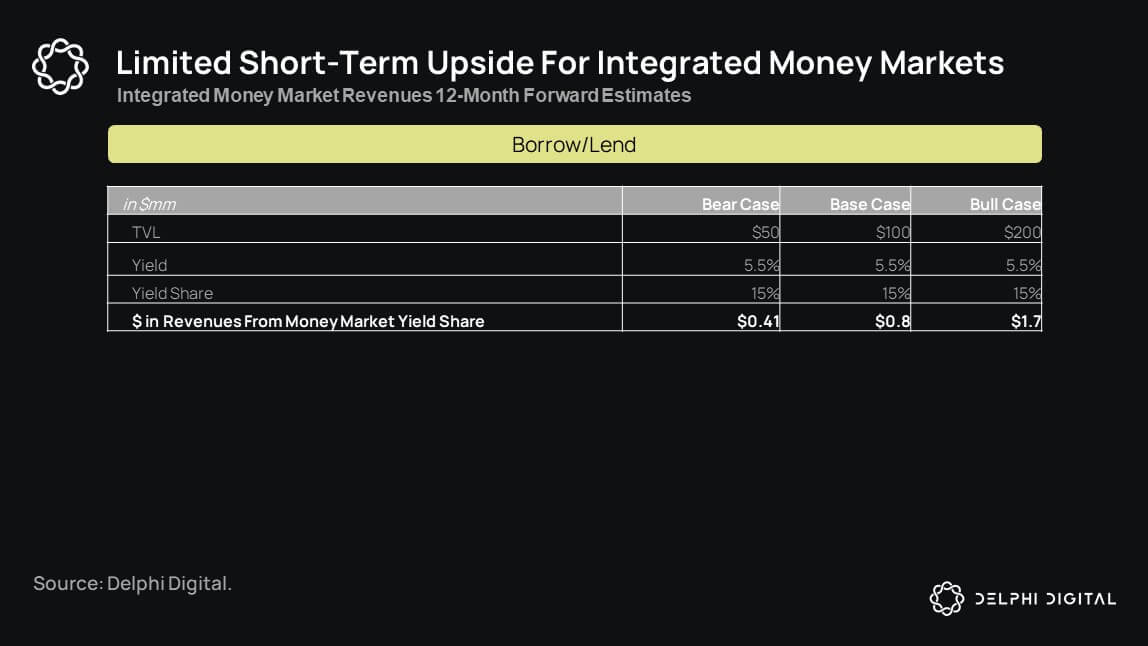

I believe, for the most part, that when users want yield on Paradex they will use the tokenized vaults and the Gigavault before using a native borrow/lend application. However, I do think this changes over time, but I think this change could take 18-36 months, therefore I assume very modest growth here.

I believe these to be large revenue streams for Paradex in the future, but I do think it will take time. Paradex is likely to take a white glove approach to helping the first few teams build out, I expect the first few to be huge successes, but again, this will take time and therefore I ascribe zero Year-1 revenue to their "non-core business" lines.

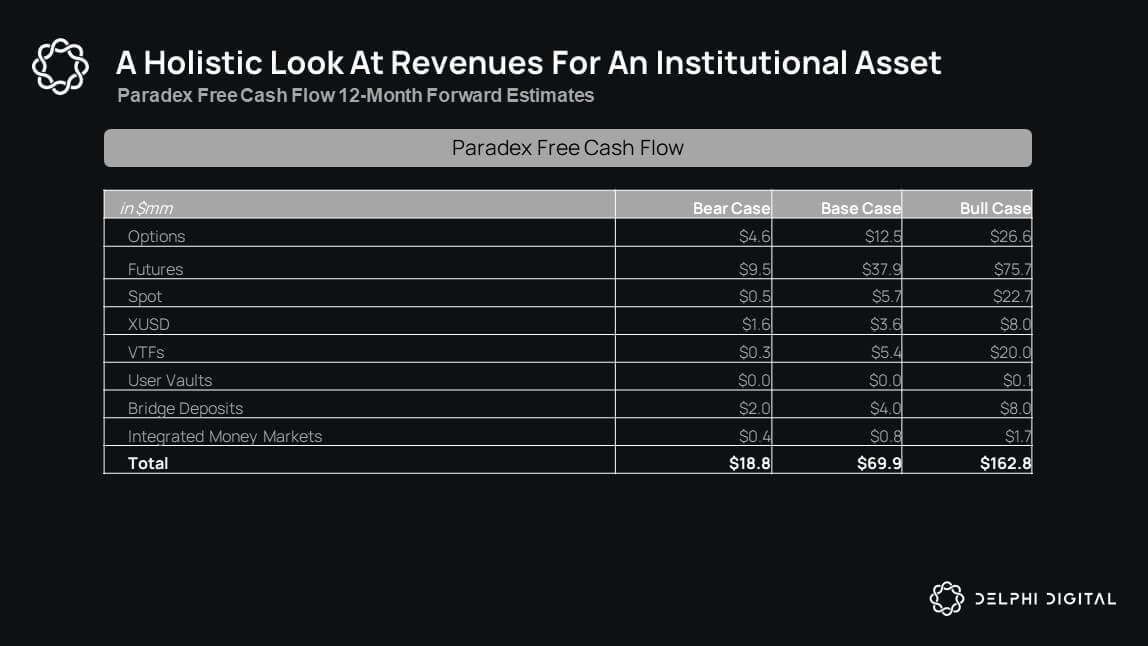

Putting it all together paints a compelling case on why, $DIME in the future, has the potential to be a favored asset by institutions. Paradex's near-term revenue may look "light" next to fee-first DEX peers, and that's deliberate. The model taxes makers, not takers: PFOF and zero taker fees, made possible by RPI flow segmentation. That choice compresses headline bps today but wins other battles – distribution via cheaper all-in execution (tighter realized spreads, zero fees, less slippage) and defensibility (makers pay to access curated, low-toxicity UI flow). As volume compounds, the broader product set, options, vaults, lending, and a Roblox-style app layer, adds bps back on a much larger base. I'd rather underwrite durable FCF from growing, nonmercenary flow than chase short-term ARPU. Everything above rolls into FCF for the P/FCF lens.

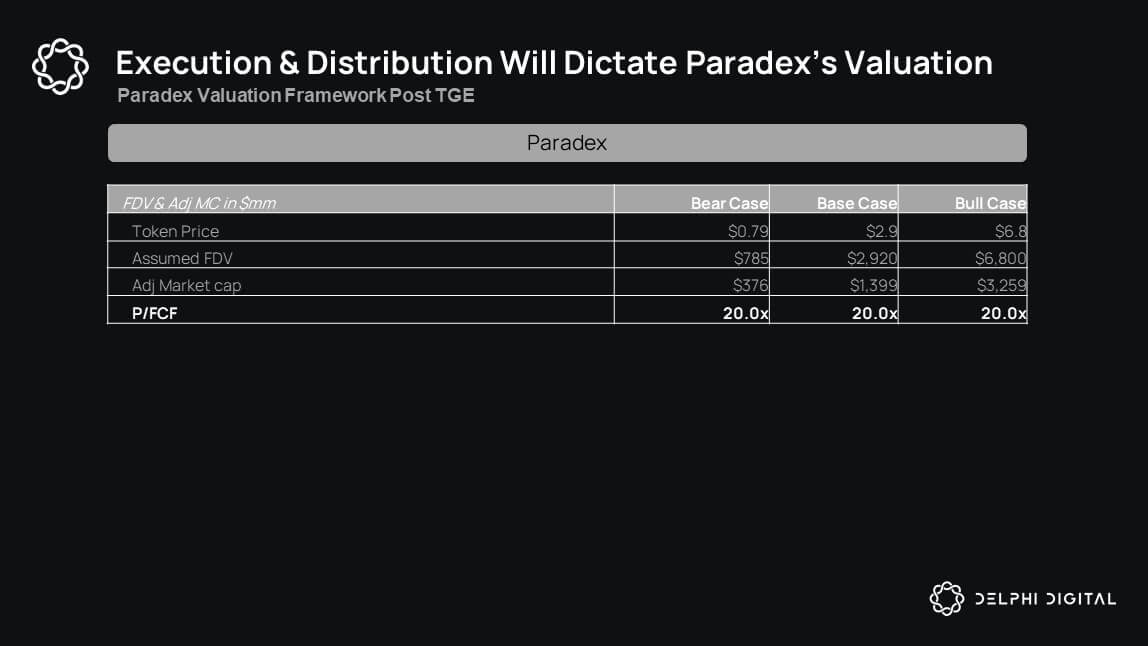

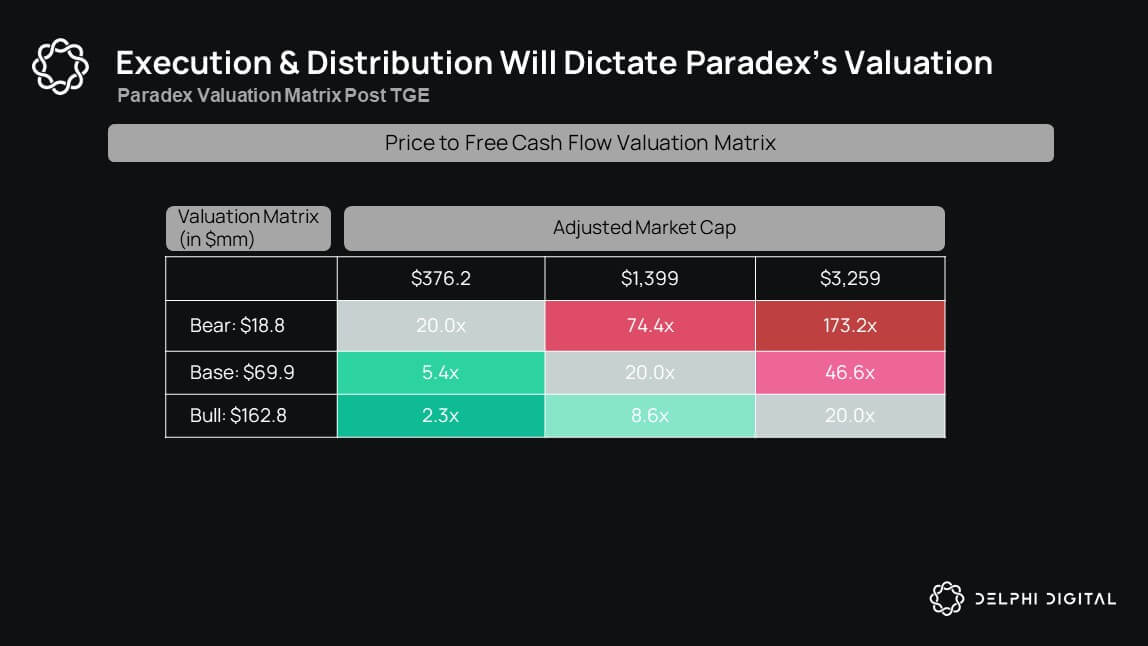

If Paradex delivers on these base assumptions, I think a ~$3B fully diluted valuation is a reasonable waypoint.

This does not mean I believe they will or should have their TGE around this valuation. In order to demand this type of valuation they will need to take meaningful market share from other perpetual exchanges including Binance. However, I do believe the founder and team have the pedigree to do so.

For those curious, here is a valuation matrix using my assumptions:

Paradex represents a high-conviction bet on a fundamentally different approach to building an exchange. It's not the easiest path and is far from consensus. The team chose more complicated technology and a more novel market structure over simply copying what came before, but if they pull it off, the result is a step-change improvement in how markets operate on-chain. And for Paradex and $DIME, the wedge would be defensible: Binance-level spreads, zero fees, plus products CeFi/DeFi hybrids don't offer natively (perp options, asset management, vault composability).

Ultimately, my thesis is that we see a zero-to-one improvement in on-chain exchange design. If we analogize to the evolution of exchanges: first-gen DeFi (Uniswap, etc.) was an innovation (AMMs vs order books), second-gen (dYdX, GMX, etc.) tried to bring more pro features but still lacked certain elements, and now Paradex is the third-gen that combines the best of CeFi and DeFi.

The execution risk remains, Paradex has to gain users and liquidity to reach critical mass. But given the scope of what they built, even moderate success could make it one of the most valuable platforms in crypto.

In a niche ecosystem where everyone else is copy-pasting Hyperliquid or spinning up another EVM chain, Paradex is a refreshing throwback to genuine first-principles thinking and deep domain expertise applied in crypto.